2026 Life Insurance: Term vs. Whole Life Employer Plans Explained

Navigating the complex world of life insurance can be daunting, especially when considering employer-sponsored plans. As we approach 2026, understanding your options – specifically the differences between term life and whole life insurance – becomes paramount to securing your financial future and that of your loved ones. This comprehensive guide will dissect these two primary types of coverage offered through employers, providing you with the knowledge to make an informed decision for your 2026 life insurance needs.

Understanding Your 2026 Life Insurance Options: Term vs. Whole Life in Employer Plans

Life insurance is a cornerstone of sound financial planning, offering a safety net for your family should the unexpected occur. Employer-sponsored life insurance plans are a valuable benefit, often providing coverage at a lower cost than individual policies. However, the choice between term life and whole life insurance within these plans can be confusing. This article aims to demystify these options, focusing on what you need to know for your 2026 life insurance decisions.

The Foundation: What is Life Insurance?

Before diving into the specifics of term and whole life, let’s briefly review the purpose of life insurance. At its core, life insurance is a contract between an insurer and a policyholder. In exchange for premium payments, the insurer pays a lump sum, known as a death benefit, to the policyholder’s beneficiaries upon their death. This benefit can be crucial for covering funeral expenses, replacing lost income, paying off debts, funding education, or maintaining a family’s standard of living.

Why Employer-Sponsored Life Insurance?

Many employers offer some form of life insurance as part of their benefits package. This often includes a basic level of coverage provided at no cost to the employee, with options to purchase additional coverage (supplemental or voluntary life insurance) through payroll deductions. The advantages of employer-sponsored plans typically include:

- Convenience: Easy enrollment and payroll deductions.

- Affordability: Group rates are often lower than individual policies.

- Guaranteed Issue: For basic coverage, medical exams are often waived. Supplemental coverage might require some health questions.

- Accessibility: Provides coverage to individuals who might otherwise struggle to obtain it due to health issues.

However, it’s essential to understand that employer-sponsored plans might have limitations, such as coverage ending if you leave the company, or the amount of coverage being capped. This makes understanding the different types of 2026 life insurance critical.

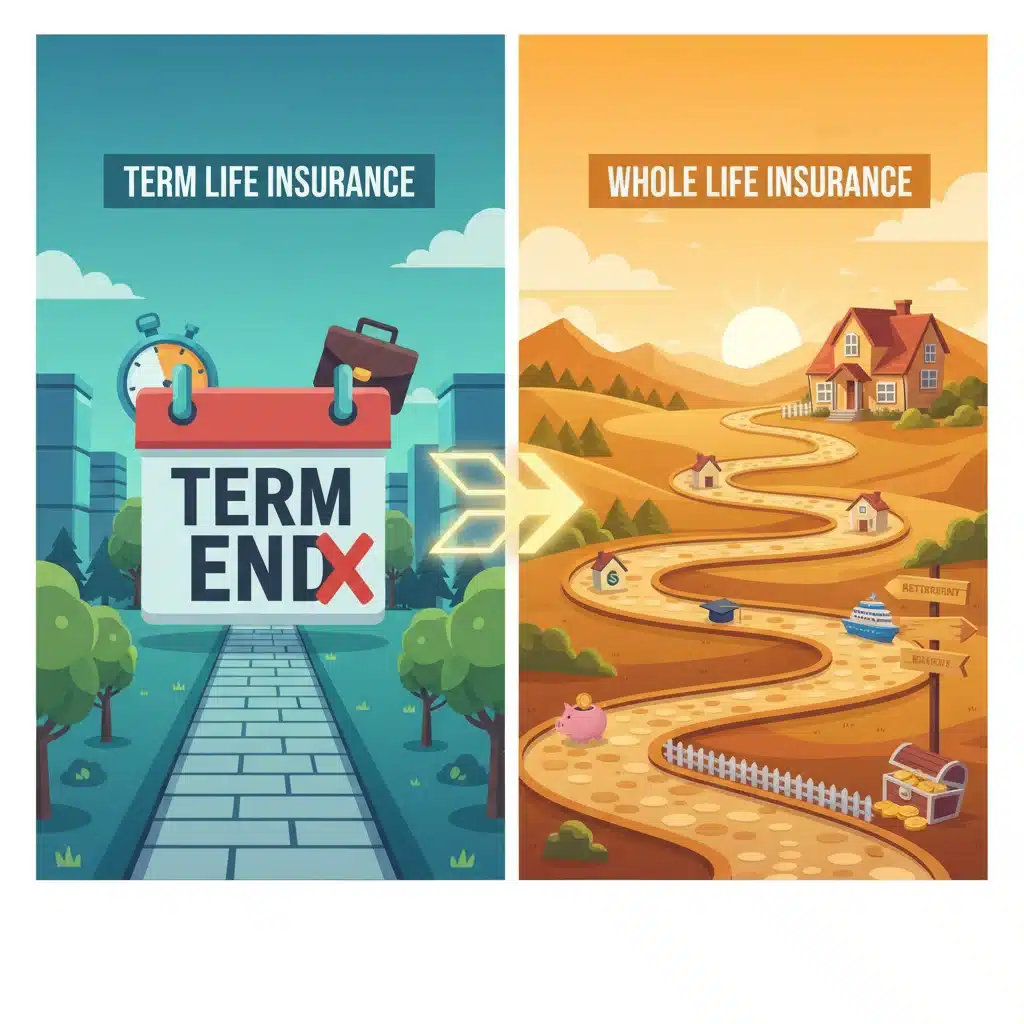

Term Life Insurance: The Temporary Safety Net for Your 2026 Life Insurance Needs

Term life insurance is often considered the more straightforward of the two options. It provides coverage for a specific period, or ‘term’ – typically 10, 20, or 30 years. If the insured passes away during this term, the beneficiaries receive the death benefit. If the term expires and the insured is still alive, the policy simply ends, and no benefit is paid. Some policies offer the option to renew for another term, often at a higher premium, or to convert to a permanent policy.

Key Characteristics of Term Life Insurance:

- Defined Period: Coverage is for a set number of years.

- Pure Protection: Primarily focuses on providing a death benefit, with no cash value component.

- Affordability: Generally less expensive than whole life insurance, especially for younger individuals, making it an attractive option for many seeking 2026 life insurance.

- Fixed Premiums: Premiums typically remain level throughout the term.

- No Cash Value: Does not accumulate cash value or offer investment opportunities.

Advantages of Term Life Through an Employer:

- Cost-Effective: Group rates can make term life very affordable, especially for basic coverage.

- Simplicity: Easy to understand and enroll in.

- Meeting Specific Needs: Ideal for covering financial obligations that have a clear end date, such as a mortgage, childcare expenses, or a child’s college education.

Disadvantages of Term Life Through an Employer:

- Temporary Coverage: The biggest drawback is that coverage eventually ends. If you still need insurance after the term expires, you’ll need to purchase a new policy, possibly at a higher rate due to age or health changes.

- Non-Portable (often): Many employer-sponsored term policies are not portable, meaning coverage ceases if you leave your job. Some might offer conversion options, but these can be more expensive.

- No Cash Value Growth: Unlike whole life, term life does not build cash value, so there’s no savings or investment component.

When considering 2026 life insurance, term life is often a good choice for those who need substantial coverage for a specific period while keeping premiums low. It’s particularly useful for individuals with young families or significant short-to-medium-term financial responsibilities.

Whole Life Insurance: The Permanent Solution for Your 2026 Life Insurance Strategy

Whole life insurance is a type of permanent life insurance that provides coverage for your entire life, as long as premiums are paid. Beyond the death benefit, whole life policies also feature a cash value component that grows over time on a tax-deferred basis. This cash value can be accessed through loans or withdrawals, offering a living benefit in addition to the death benefit.

Key Characteristics of Whole Life Insurance:

- Lifetime Coverage: Remains in force for your entire life.

- Cash Value Accumulation: A portion of your premium goes into a cash value account that grows guaranteed.

- Fixed Premiums: Premiums are typically level for the life of the policy.

- Guaranteed Death Benefit: The death benefit is guaranteed as long as premiums are paid.

- Living Benefits: Policyholders can borrow against or withdraw from the cash value.

Advantages of Whole Life Through an Employer:

- Permanent Protection: Provides lifelong peace of mind, ensuring your beneficiaries will receive a payout regardless of when you pass away. This is a significant consideration for long-term 2026 life insurance planning.

- Cash Value Growth: The guaranteed cash value growth can act as a forced savings mechanism and a source of liquidity later in life.

- Tax Advantages: Cash value growth is tax-deferred, and death benefits are generally income tax-free.

- Portability (often): Employer-sponsored whole life policies are often portable, meaning you can take them with you if you change jobs, maintaining continuous coverage.

Disadvantages of Whole Life Through an Employer:

- Higher Premiums: Due to the lifelong coverage and cash value component, whole life premiums are significantly higher than term life premiums for the same death benefit.

- Less Flexibility: Premiums are fixed, and the growth rate of the cash value is often modest compared to other investment vehicles.

- Complexity: Can be more complex to understand than term life policies.

For those looking for a permanent solution and who value the cash value component and guaranteed growth, whole life insurance, even through an employer plan, can be a valuable part of their 2026 life insurance portfolio.

Comparing Term Life and Whole Life for Your 2026 Life Insurance Strategy

To help you decide which type of 2026 life insurance is right for you, let’s directly compare term and whole life insurance across several key aspects:

Cost

- Term Life: Lower initial premiums, making it more accessible for many budgets.

- Whole Life: Significantly higher premiums due to its permanent nature and cash value component.

Coverage Duration

- Term Life: Coverage for a specific period (e.g., 10, 20, 30 years).

- Whole Life: Lifelong coverage.

Cash Value

- Term Life: No cash value accumulation.

- Whole Life: Builds cash value over time, which can be accessed by the policyholder.

Purpose

- Term Life: Ideal for covering specific, temporary financial needs (e.g., mortgage, children’s education).

- Whole Life: Suitable for lifelong financial planning, estate planning, and providing a guaranteed legacy.

Flexibility

- Term Life: Can be converted to permanent insurance, but usually at a higher cost.

- Whole Life: Offers less flexibility in terms of premium adjustments but provides access to cash value.

Making the Right Choice for Your 2026 Life Insurance

The best choice for your 2026 life insurance needs depends on your individual circumstances, financial goals, and budget. Here are some questions to consider:

1. What are your financial obligations?

- If you have significant debts (mortgage, car loans) or dependents whose financial well-being relies on your income for a specific period, term life might be sufficient.

- If you want to ensure a death benefit for your entire life, perhaps for estate planning or to leave a legacy, whole life is more appropriate.

2. How long do you need coverage?

- If you anticipate your major financial responsibilities will end within a certain timeframe (e.g., children become independent, mortgage is paid off), term life may fit your needs for 2026 life insurance.

- If you desire coverage that will never expire, whole life provides that permanence.

3. What is your budget?

- If affordability is a primary concern and you need maximum coverage for the lowest premium, term life is generally the better option.

- If you have more disposable income and want the added benefits of cash value growth and lifelong coverage, whole life might be a worthwhile investment.

4. Do you value a savings component?

- If you prefer to keep your insurance and investments separate, term life allows you to invest the difference in premiums elsewhere.

- If you appreciate the guaranteed, tax-deferred growth of a cash value component within your insurance policy, whole life offers this feature.

5. What happens if you change jobs?

- Many employer-sponsored term policies are not portable. If you rely solely on this coverage, you might find yourself uninsured or facing higher costs for new coverage upon job change.

- Employer-sponsored whole life policies are often portable, providing continuous coverage regardless of your employment status. This can be a significant benefit when considering your long-term 2026 life insurance strategy.

Maximizing Your Employer-Sponsored 2026 Life Insurance Benefits

Regardless of whether you choose term or whole life, there are strategies to maximize your employer-sponsored 2026 life insurance benefits:

1. Understand Your Basic Coverage

Most employers provide a basic, no-cost life insurance policy, often a multiple of your salary. Understand this benefit first, as it forms the foundation of your coverage.

2. Evaluate Supplemental Options

Employers often allow you to purchase additional coverage. Compare the rates and terms of these supplemental policies with what you could get individually. Sometimes, employer group rates are highly competitive.

3. Don’t Rely Solely on Employer Coverage

While convenient, employer-sponsored plans might not be enough. If you have significant financial responsibilities, consider supplementing your employer coverage with an individual policy. This ensures you have adequate protection that is fully portable and tailored to your specific needs, independent of your employment.

4. Review Annually During Open Enrollment

Your life circumstances change – you might get married, have children, buy a house, or get a promotion. Open enrollment is the perfect time to review your 2026 life insurance needs and adjust your coverage accordingly. This is especially true as you plan for 2026 and beyond.

5. Understand Portability and Conversion Options

Before enrolling, know what happens to your policy if you leave your job. Can you take it with you (portability)? Can you convert a term policy to a whole life policy without a medical exam? Understanding these options is crucial for long-term planning.

6. Nominate and Update Beneficiaries

Ensure your beneficiaries are up-to-date. Life events like marriage, divorce, or the birth of a child necessitate reviewing and updating your beneficiary designations. This is a critical step to ensure your death benefit goes to the intended recipients.

Key Considerations for Your 2026 Life Insurance Planning

As you plan for your 2026 life insurance, keep these broader considerations in mind:

Inflation and Coverage Amount

The cost of living generally increases over time due to inflation. When determining your coverage amount, consider how much your family would need in the future, not just today. A death benefit that seems sufficient now might not be adequate in 10 or 20 years.

Health Changes

Your health status can significantly impact the cost and availability of life insurance. Locking in coverage while you are younger and healthier can provide substantial long-term savings. If you anticipate health changes, securing permanent coverage sooner rather than later could be advantageous.

Riders and Additional Benefits

Many policies, both term and whole life, offer riders – additional benefits that can be added to a policy. These might include:

- Waiver of Premium Rider: Waives premiums if you become disabled.

- Accidental Death Benefit Rider: Pays an additional benefit if death is due to an accident.

- Children’s Term Rider: Provides a small amount of term coverage for your children.

- Accelerated Death Benefit Rider: Allows you to access a portion of your death benefit early if you are diagnosed with a terminal illness.

Reviewing available riders can enhance the value of your 2026 life insurance policy.

Professional Financial Advice

While this guide provides a solid foundation, individual situations are unique. Consulting with a qualified financial advisor can help you assess your specific needs, integrate life insurance into your broader financial plan, and navigate the nuances of employer-sponsored benefits versus individual policies. They can offer personalized recommendations for your 2026 life insurance strategy.

Conclusion: Securing Your Future with Smart 2026 Life Insurance Choices

Choosing between term life and whole life insurance within your employer’s benefits package for 2026 life insurance is a critical decision that impacts your financial security and peace of mind. Term life offers affordable, temporary coverage for specific needs, while whole life provides lifelong protection with a cash value component. Both have distinct advantages and disadvantages, and the ‘best’ option is truly personal.

By thoroughly understanding the characteristics of each, evaluating your financial situation, and considering your long-term goals, you can make an informed decision. Remember to review your coverage regularly, especially during open enrollment periods, and consider supplementing employer-sponsored plans with individual policies if your needs dictate. Proactive planning for your 2026 life insurance will ensure your loved ones are protected, no matter what the future holds.